5 Surprising Findings From Our Covid-19 Compliance Survey

The world has changed and compliance along with it. In this week’s StarBlog, you’ll get a taste of what our new e-book has in store and also be able to download it for FREE

On April 21, 2020, our survey of compliance professionals from across the world of finance hit the streets, asking questions we believe got at the heart of the unexpected and continuing challenges surrounding keeping individual employees and firms compliant in the new normal of remote work.

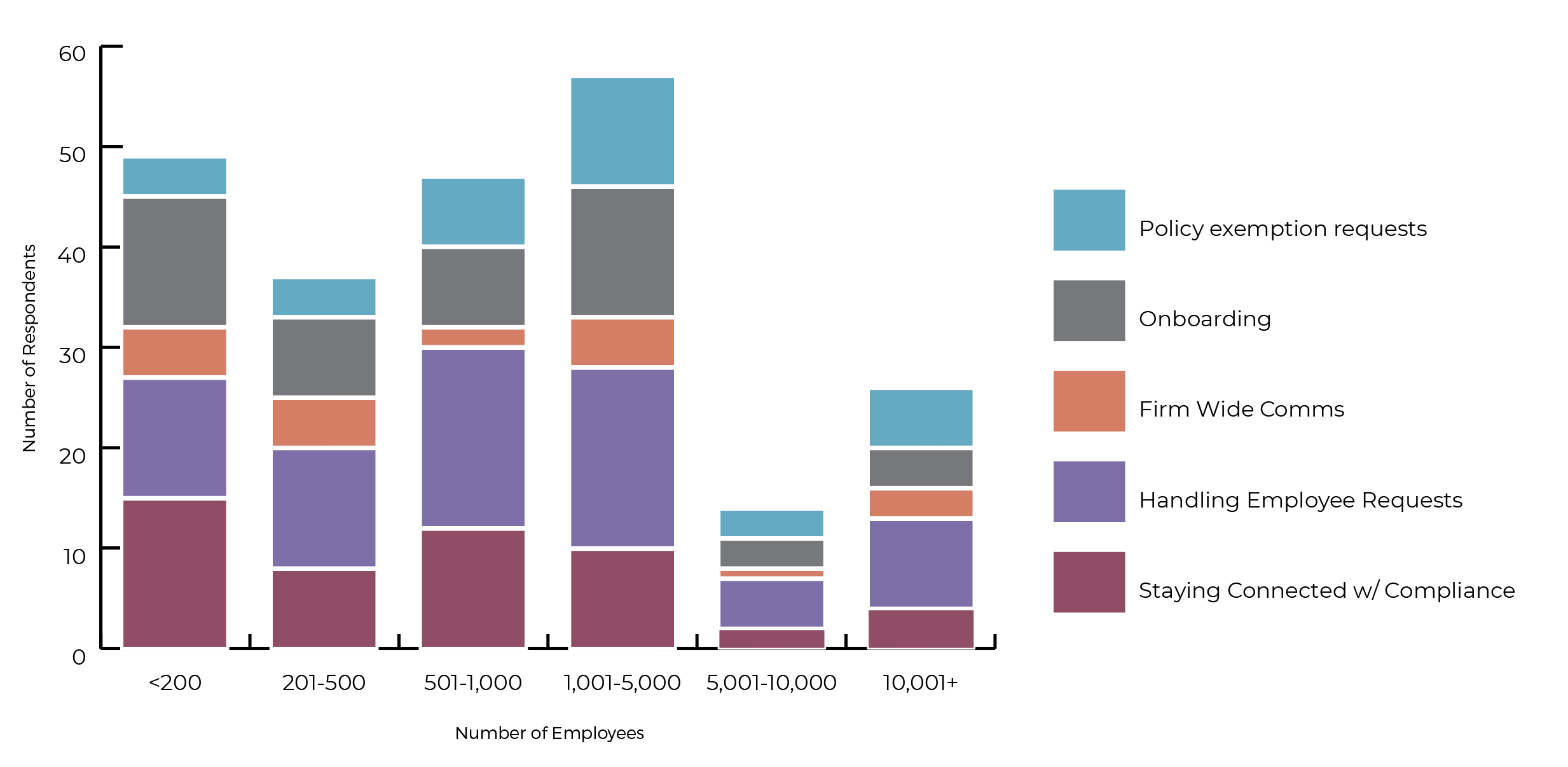

The survey garnered responses from more than 160 firms, running the gamut in size from less than 200 to more than 10,000 employees. Firm types included Asset Managers, Private Equity, Broker-Dealers, and Investment Banks. Regions surveyed included North America (NA), EMEA, APAC, and the UK.

We’ve compiled these responses in our new e-book—Coping With COVID: Survey Findings Of The Impact On Global Compliance. It goes into great detail on the survey’s findings, and also incorporates insights and commentary from the team at StarCompliance. You can download this FREE e-book in its entirety now. To get a taste of what the e-book has in store, check out the following five surprise findings from this benchmark survey.

1. MORE REQUESTS, MORE REVIEWS

Across all four geographic regions, 43% reported the biggest challenge overall was handling employee requests. By employee size, the largest firms also noted this as the top challenge. It makes sense that more employees mean more requests, and the data bears this out: on average 36% of the largest firms also experienced three to four times more trading activity.

While one would think bigger firms would have the technological and human resources at their disposal to handle such a surge, the increase in pre-clearance requests—combined with the increased number of shares employees wished to trade—likely triggered more reviews because the shares were above the standard trading threshold firms had built into their pre-clearance automation. As a result, perhaps even the most capable systems and well-considered processes are feeling the strain of it all.

2. ASK AND YOU SHALL NOT RECEIVE

Despite recent FCA and PRA guidance offering some room to maneuver when it comes to regulatory enforcement during the coronavirus pandemic (read Star’s coverage here and here), firms are generally not allowing significant exemptions from their existing policies during this period (read Star’s coverage here)—feeling it’s more important than ever to maintain effective policies and controls, as regulators will undoubtedly be back at it, and looking for any slip-ups, when things return to a more normal state.

It will come as little surprise, then, that only 22% of survey respondents overall identified policy exemption requests as a challenge. Of note, however, is the 40% of EMEA-only located firms that chose policy exemption requests as their top challenge. It seems EMEA employees may have been more willing to ask for exemptions, though most were likely still rejected. This may be because EMEA compliance programs and regulations surrounding personal account dealing are simply not as prescriptive as in other regions, like NA and the UK. Overall, both UK and US firms have been reluctant to grant exemptions at this time.

3. PROGRESS, AND PROJECTS, MARCH ON

Given the ongoing pandemic and knock-on economic effects, news from the survey that there have been significant delays to financial compliance projects would have been expected. Just the opposite was reported, however. While there have been some delays to 2020 compliance projects and initiatives, more than 60% of firms report that programs have been able to continue, and firms are currently not forecasting significant delays to compliance projects, initiatives, and improvements. This is notable.

A positive take on this is, while industries and businesses across the globe are cutting spending in order to remain cash positive, the financial industry remains steadfast in its resolve for the continuation and improvement of compliance processes by supporting related initiatives and improvements. In fact, some firms may be of the opinion that compliance initiatives are now even more important because of new risk factors created by the pandemic, like increased trading activity and remote working.

4. COMPLEXITY NEEDS PROXIMITY

Distributing policies to new employees and having them complete tasks is likely a straightforward affair for compliance departments: something that can be done relatively easily via electronic means for those working remotely. But communicating the why of the policies—and other more subtle information about firm culture and expectations—is a bit harder to do via an email chain.

Overall, 30% of respondents chose onboarding new employees as a significant challenge during the COVID crisis. And 50% of both Investment Banks and Stock Exchanges expressed this as a top challenge, more so than any of the other industries surveyed. Being such closely related industries—both highly complex and highly regulated—it’s not hard to imagine that communicating the nuances of firm culture, policy prescription, and regulatory rigor is most effective when delivered in-person. So while technology can solve for most things in the current environment, it seems the human element is still a necessary one.

5. CENTRALIZING SOFTWARE IS KEY

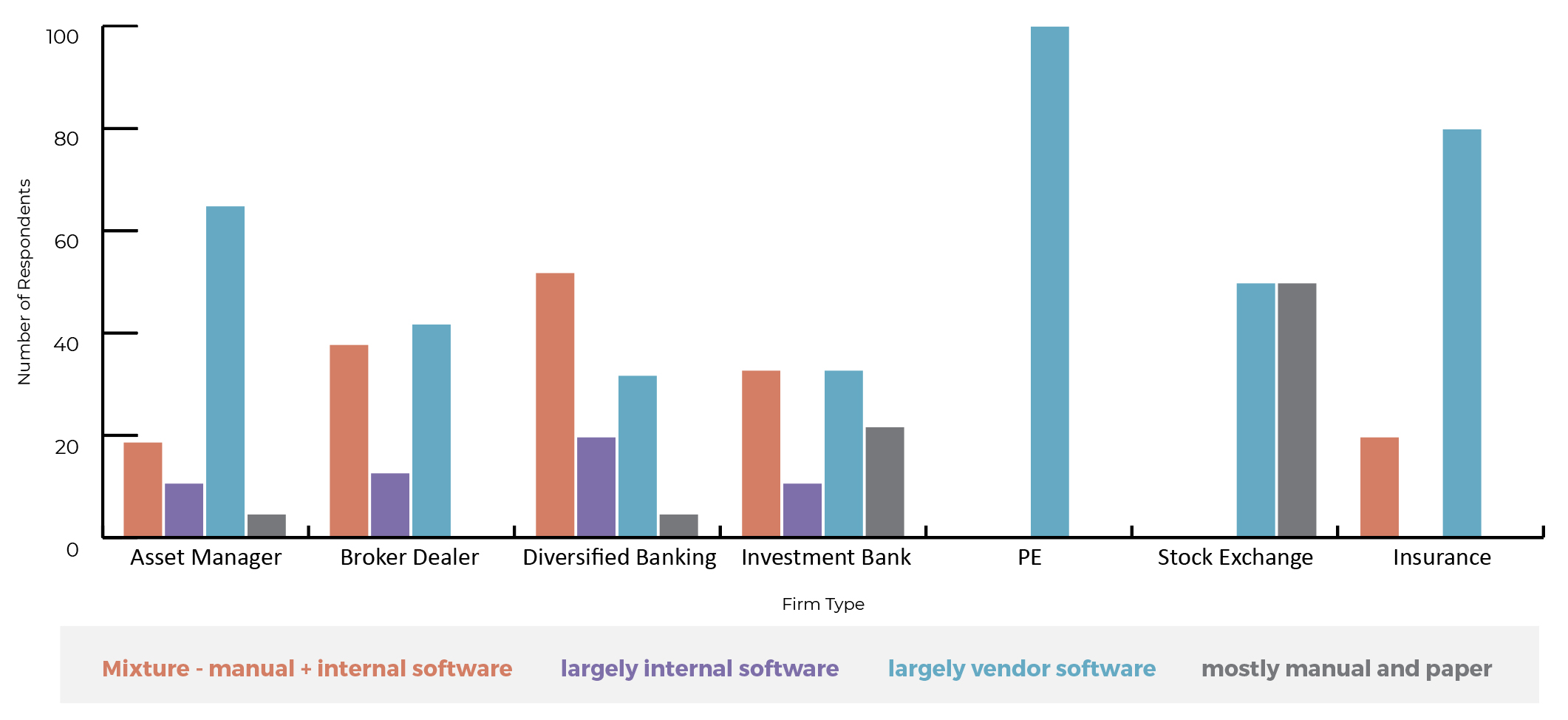

More than 50% of survey respondents indicated they have a centralized, compliance software system in place, whether built and maintained in-house or vendor-sourced. Over 70% of all Asset Managers and 55% of all Broker-Dealers reported using either largely internally developed software or largely vendor software, and over 65% of both industries believe their compliance processes are very effective.

These firms continued to have effective compliance monitoring and certifications processes throughout the COVID-19 crisis. The ability to automate trade monitoring, certifications, attestations, and internal communications surrounding all these workflows has made it easier to adjust to keeping tabs on a remote workforce. However a firm chooses to get there—be it via in-house or vendor software—a modern compliance platform that can do all of the above and more is going to be of enormous help anytime. In the middle of a pndemic no one saw coming, with knock-on effects no one dreamed of, it’s proving to be invaluable.

These firms continued to have effective compliance monitoring and certifications processes throughout the COVID-19 crisis. The ability to automate trade monitoring, certifications, attestations, and internal communications surrounding all these workflows has made it easier to adjust to keeping tabs on a remote workforce. However a firm chooses to get there—be it via in-house or vendor software—a modern compliance platform that can do all of the above and more is going to be of enormous help anytime. In the middle of a pndemic no one saw coming, with knock-on effects no one dreamed of, it’s proving to be invaluable.

Enterprise Conflicts Handbook