Consumer Duty: Why Individual Accountability and Training & Competency Solutions Matter

In the UK, the Financial Conduct Authority (FCA) is looking to bring higher and clearer standards of consumer protection in retail financial services through…

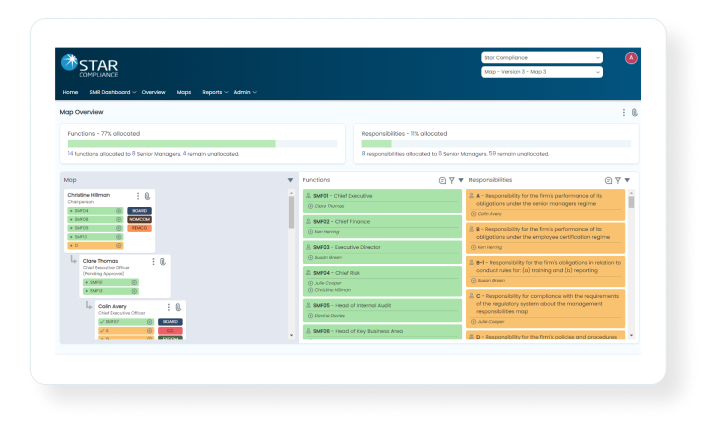

Designed for in-scope FIs to establish and maintain a Senior Manager’s Regime and adapt to changes in regulation as they occur.

Be certain you’re complying with the Financial Conduct Authority’s (FCA) guidance on the Senior Manager & Certification Regime (SMCR) with a solution that’s designed to meet the United Kingdom’s regulations and any future guidance.

Comply with Australia’s BEAR and FAR accountability frameworks with confidence.

Maintain a compliant Individual Accountability and Conduct (IAC) program aligned with MAS regulations.

Stay aligned with the Central Bank of Ireland’s Individual Accountability Framework requirements.

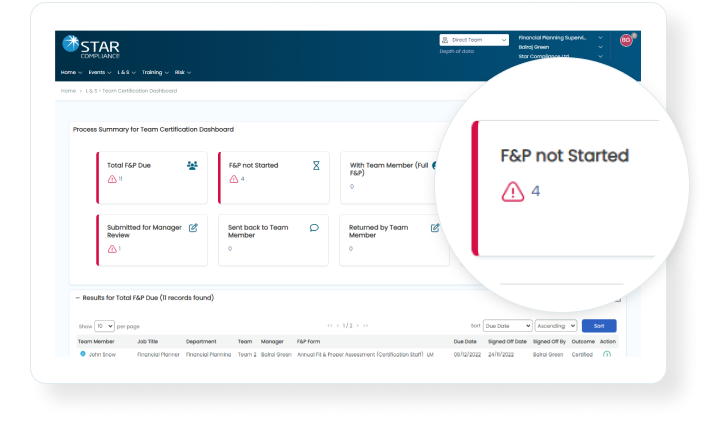

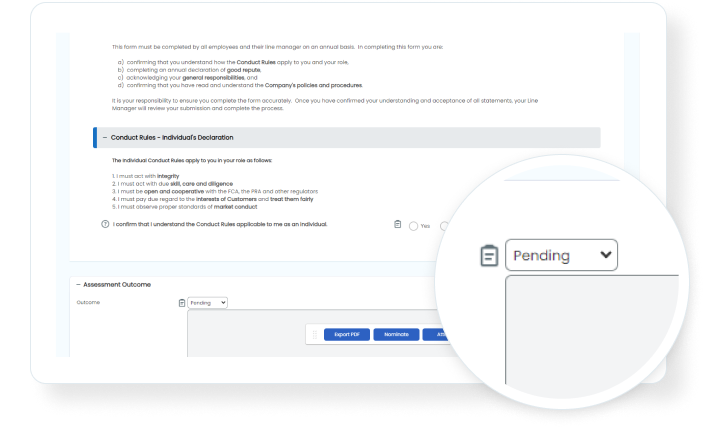

Gain control of all aspects of the certification process – with compliance technology that makes it easy for your employees.

Raise awareness of employee conduct issues across your firm and expand individual accountability. Fostering a culture of strong values and ethical behaviour is what builds respected, reputable businesses.

Make it easy to support the regular submission and maintenance of up-to-date data for FCA Directory Persons, providing a place to gather and store data, as well as ensuring changes and updates are applied on time and consistently.

Designed for compliance and HR departments alike, our solutions simplify everyday compliance processes while ensuring you meet the strictest regulatory and ethical standards. STAR is highly configurable, providing a personalized experience to all end users that increases adoption and keeps your individual accountability program running smoothly.

Extensive workflows are highly configurable, powered by conditional logic.

Tailor time zone, currency, language, and more for global employees.

Drive employee adoption with ease and simplify employee access via standard authentication and/or single sign-on.

Quickly and easily get real-time analytics through customizable dashboards and reports.

Safeguard sensitive data with multi-layered access rights based on division, department, role, location, and more.

Gain a 360-degree view of your employee compliance anywhere with scalable, cloud-ready software and integrations with Snowflake, Thoughtspot, and PowerBI.

In the UK, the Financial Conduct Authority (FCA) is looking to bring higher and clearer standards of consumer protection in retail financial services through…

In our second blog examining the compliance outlook for financial services firms in 2023, Gary Muchmore, Managing Director at StarCompliance, discusses upcoming legislation for…

The Central Bank of Ireland is making the case for better firm governance through better firm culture.